No More Hustleporn: What Is The Durbin Amendment

Tweet by Samir

https://twitter.com/heysamir_/

Fintech startup advisor + investor | Over-engineered fintech tweets every other week | Previously StratFin @Chime, Finance @Sift, Banking @JPMorgan | @Duke alum

1/16 Spend enough time in neobanking fintech & you'll inevitably hear somebody talk about the "Durbin Amendment".

It's the reason every neobank exists AND the biggest dependency risk to their business model.

But what if I told you the downside risk isn't as bad as it seems?

2/16 It all comes back to interchange.

What you should know is that post financial crisis, the Durbin Amendment* set up two rate cards for what debit interchange rates banks could charge merchants.

*For more on Durbin Amendment lore, see @patio11's post:

3/16 The rate card seems pretty simple:

#1. Banks > $10B in assets (Durbin Regulated): interchange rate is capped at $0.22* + 5bps

#2. Banks < $10B in assets (Durbin Exempt): interchange rate is uncapped and follows network interchange tables

*Includes 0.01 for fraud prevention

4/16 Many think the Durbin Amendment is untouchable. Who could be against a rule that lowered txn costs for merchants w/ all big banks (#1) and let community banks & neobanks compete against big banks w/ debit products (#2)?

None other than Dick Durbin.

5/16 While rate card part of Durbin hasn't changed yet, merchants are pushing on another section that requires two unaffiliated networks for txn routing (Sig & PIN w/ PIN being cheaper). It only applies to POS, but merchants want it to apply online too.

6/16 So Durbin Amendment may not seem as untouchable as we thought.

But what actually happens if Durbin exemption goes away and all banks have capped interchange?

Sounds like we can just check those interchange tables and find out right?

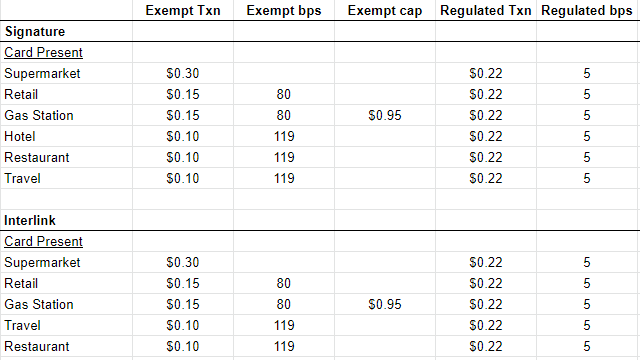

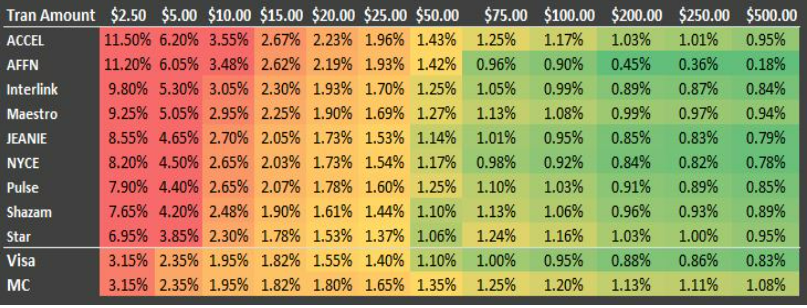

7/16 Well, they're complex but I bet fintech nerds saw @Visa Consumer Check Card (Durbin Exempt) rate is ~$0.15 + 80bps.

So on $100 txn:

$0.15 + 80bps (Exempt) is $0.95

$0.22 + 5bps (Regulated) is $0.27

So neobanks lose 71% interchange w/o Durbin?

That is where you're wrong.

8/16 Because of avg txn size, card presence, category mix, Sig vs PIN, *neobanks likely lose < 36% debit interchange even w/o Durbin*.

It would hurt, but doesn't kill.

But how?

I dug through data on these 4 factors to show how the unit economics of interchange play out 👇🏾👇🏾

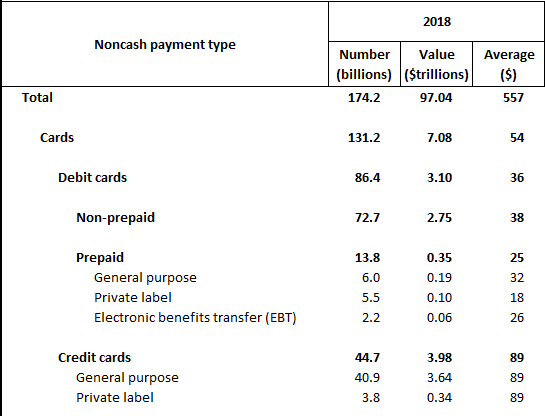

9/16 #1 *Average Transaction Size*

Since interchange rates have a fixed fee & a variable fee, ATS matters a lot. Lower ATS means variable fee has a smaller impact on overall costs.

And debit is way lower than credit: only ~$36.

Among debit, PIN ($41) higher than Sig ($31)

10/16 #2 *Card Presence*

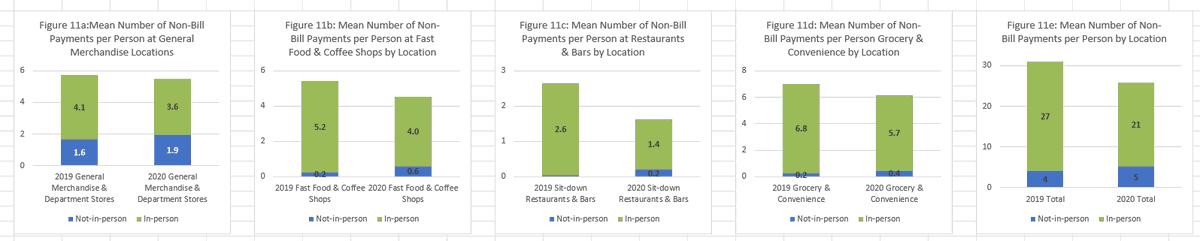

Swiping your debit online (card-not-present CNP) vs. in store (POS / card present) means higher interchange b/c it can be riskier for network to support these txns. Also online spend is Sig only for now which is also higher interchange.

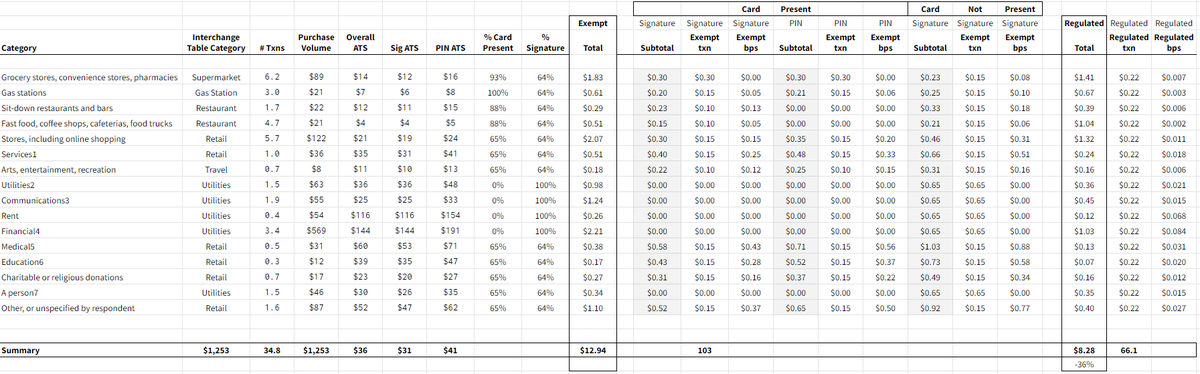

11/16 #3 *Category Mix*

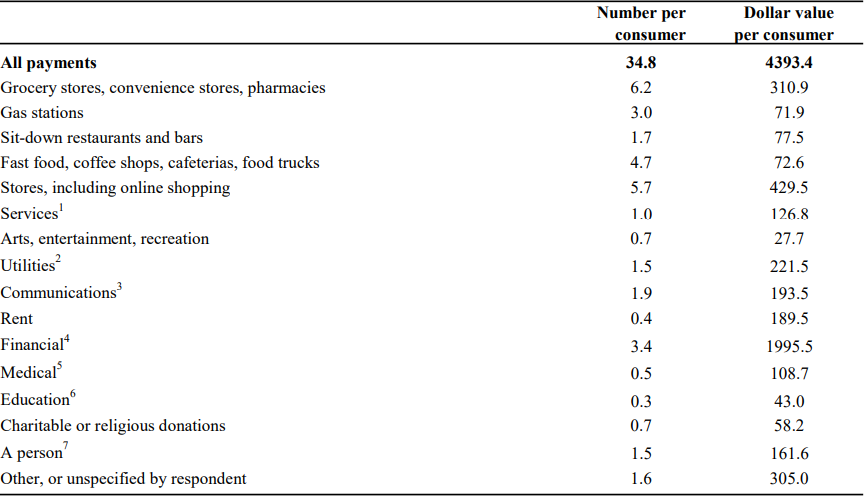

Where you spend also affects interchange b/c of category ATS and category-specific (and sometimes merchant-specific) interchange rates.

NOTE - Chart shows ALL payments mix but we'll assume similar mix for Debit and normalize ATS using overall Debit ATS.

12/16 #4 *Signature vs. PIN*

Signature and PIN are two different network rails, they could have diff interchange rates & PIN usually cheaper on blended basis.

Fun fact though - Visa Sig vs. PIN (Interlink) rates are basically the same.

So how is PIN cheaper overall?

13/16 Because of Durbin, there has to be 2 *unaffiliated* networks supported, so if you're a Visa neobank for example, you might have Visa Sig, Visa PIN and one other PIN network to follow the rules.

Merchants route lowest cost and most PIN networks are cheaper at higher ATS.

14/16 So, we have ATS, card presence, Sig vs PIN* & category mix. Then we map categories to interchange rates & calc blended interchange.

The result: ~36% less interchange w/o Durbin (vs. 71% expected).

*For simplicity, using Visa Sig & 1 PIN network (Interlink) vs. multi-PIN

15/16 Look - no neobank is excited about losing *only* 36% of their interchange. That's still BIG.

But we can give neobanks some slack on the doomsday scenario b/c even this unlikely situation, all is not lost. And product diversification (incl. credit) mitigates further.

16/16 And that's a wrap! If you like this thread go back up to the top and give it a like, comment, or retweet.

I try to write over-engineered fintech and crypto threads every 1-2 weeks so follow me @heysamir_ for more nerdery coming soon! References:

1. SF Fed Payments Diary - frbsf.org/cash/publicati…

2. ATL Fed Payments Diary - atlantafed.org/banking-and-pa…

3. Fed Payments Study - federalreserve.gov/paymentsystems…

4. @unit_co_ Interchange Guide - unit.co/guides/ultimat…

5. Visa Interchange Rates - usa.visa.com/content/dam/VC…

.gif)

Unit | Ultimate Guide to Interchange Revenue

Diary of Consumer Payment Choice