Semiconductors

Tweet by Jordan

Investing and writing longform @ http://vineyardholdings.net || Learning about semiconductors, China, & DeFi.

1/ With all the hype around 4IR, IoT and AI, I thought I’d spend some time digging into the tech underpinning these trends: Semiconductors.

Here’s a quick beginner’s thread overviewing the industry, its members and the trends. 2/ Made of silicon, semis underpin most modern electronics.

They are essentially incredibly small bits of conductive material that form the basis for integrated circuits – the little chips you see in laptpos, computers, cell-phones etc. 3/ While the final design of semiconductors varies according to their purpose, the initial phase of creating the semi is pretty standard. 4/ The industry is split into companies which design the chips, and those which fabricate them.

Some companies do both (Samsung/Intel), but most only do one or the other. Then there are support companies which provide equipment/testing. 5/ Fabricating a semiconductor is an incredibly costly and complex process of:

a)Perfecting & slicing silicon crystals into wafers,

b)Oxidizing the surface of the wafer

c)Creating patterns on the circuity through photolithography 6/ Steps C through E are more design specific:

d)Etching and embedding the patterns with plasma.

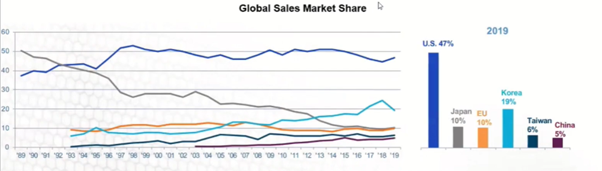

e)Injecting impure atoms into the system to give it its properties. 7/ Currently, the US has by far the dominant market share in global sales.

This is something China is looking aggressively to remedy and is one of the reasons why Taiwan (home to TSMC) is such a geographical tension-point.

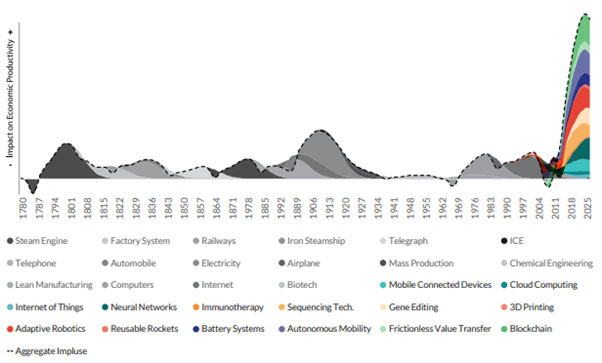

8/ Alright dude, but what’s going to make it grow?

Well, this is where it gets interesting. Smart factories, supply chain IoT, AI, cloud adoption, a 5G replacement cycle for smart devices, driving-assistance systems and big data are all buzzwords driving this industry.

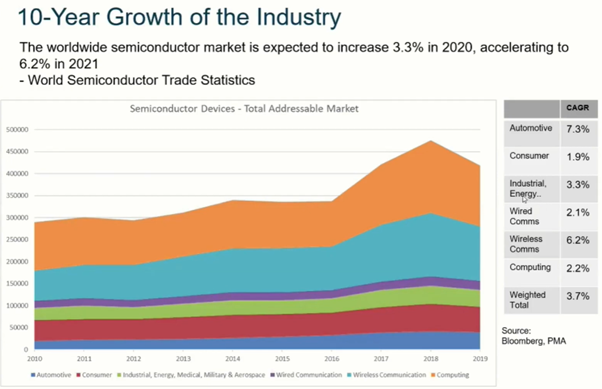

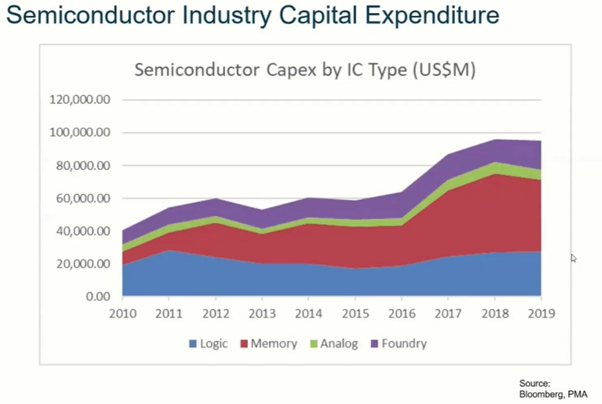

9/ It’s a pretty cyclical industry as suppliers tend to over-cater for demand rather than have shortages, which creates cyclical mis-matches between supply & demand.

Also, it’s a capex intensive industry with new tech spend required with each progressive step in improvement.

10/ Just as capex has grown for those in the industry, so too have their revenue and share prices – chaps have outpaced the S&P by a comfortable margin over the last couple years.

Mostly, this is because of increasing demand from the things in (8).

11/ Because it’s such a capital-intensive industry, the weak have got weaker while the strong get stronger. This tends towards winner-take-most oligopolies and consolidation.

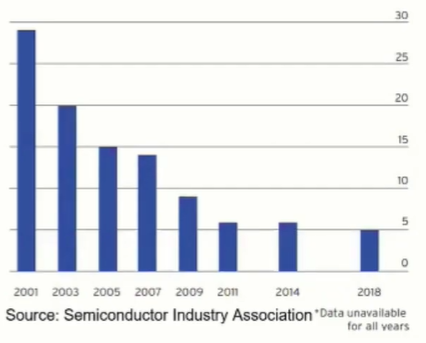

12/ In 2001, there were nearly 6x as many fabricator firms.

Many have either been acquired or run out, and fabless players would prefer to partner with a foundry than to invest in developing capabilities to manufacture their own chips.

13/ Wait. Fabless? What?

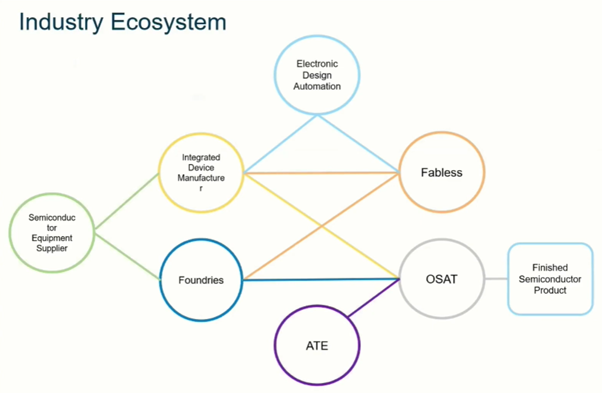

As mentioned above, the industry is divided into mostly those who manufacture (or "fab"), and mostly those who design.

Those who do both are called Integrated Device Manufacturers (IDMs), those who design: fabless, and those who fabricate: foundries.

14/ As before, there are also suppliers who manufacture equipment used in both design & fabrication of semis.

On the periphery, there are some who provide software for designing the systems, some who make testing equipment for semis & some who offer packaging/testing services.

15/ So, while it sounds complex, fortunately there are really only a handful of players to understand.

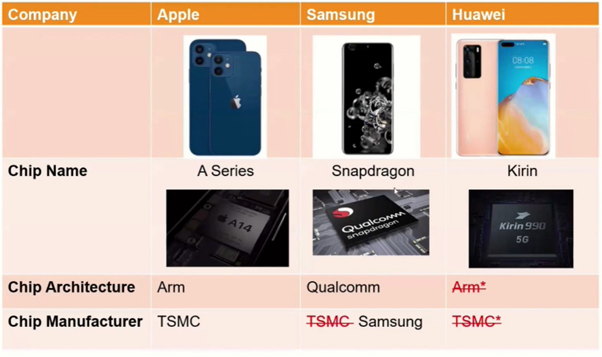

From the IDM side companies like Intel, Samsung and NXP Semis all design and fab semis internally.

Intel makes chips for laptops/PC, Samsung for phones and NXP for 4IR.

16/ While IDMs typically enjoy higher margins, they have to upgrade all their systems at a high cost whenever the next gen semi comes out.

eg: for Intel to move from the 14nm process to the 10nm process, their operating margins have struggled. Classic Innovator’s Dilemma.

17/ The fabless business model is one which designs and sells semis but outsources the fabbing to a foundry.

NVIDIA is one such company, outsourcing to TSMC. While they’ve typically aimed for GPUs used in gaming, they’re increasingly used for AI training.

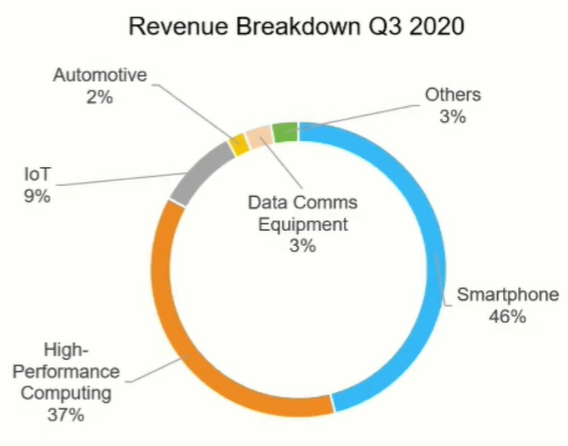

18/ We’ve spoken a lot about foundries. These are the companies which manufacture the semis/integrated circuits, but do not do the design.

Of these, Taiwan Semiconductor Manufacturing Company (TSMC) has the lions share by far.

Here’s an outline of their revenue from Q3 2020.

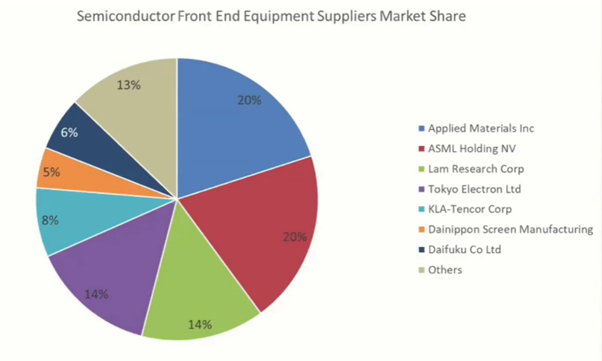

19/ Supporting the IDMs, fabless and foundries, are the equipment suppliers.

The equipment required to do the fabbing is highly sophisticated, so each of these suppliers specializes in a particular niche of equipment.

20/ The new manner of manufacturing is to use ultraviolet lithography machines (EUVs). If that sounds like a mouthful, it is.

Here’s a lekker video from @ShaneAParrish, @bjohns3 and @jbathgate describing the manufacturing process.

21/ Currently, TSMC owns roughly 50% of all EUV machines out there – giving it a leg up in the latest round of supply equipment.

Similarly, ASML is the only manufacturer of EUV machines, which – from a supply side – gives them a step up over competitor Applied Materials.

22/ Lam Research is one of the equipment supply companies who are also caught on the back foot by EUVs.

Lam specializes in etching & deposition equipment (think back to the steps for manufacturing these chips above).

EUVs ultimately shrink the TAM of traditional etch products.

23/ The last three groups of suppliers are those in electronic design automation (EDA), automatic test equipment (ATE) and outsourced semiconductor assembly and testing (OSAT).

These are typically smaller companies and will warrant another thread diving into them.

24/ To finish up, the three big trends in the industry are

a) the continued consolidation (eg NVIDIA just bought Arm for USD40b from Softbank),

b) the rise of the fabless models (mostly given the cost of fab capex) and

c) the shift of manufacturing share away from the US.

25/ In 2019, all six new semi fabs opened were outside the US, with four being built in China. It is clearly a strategic imperative of the CCP to reduce Chinese reliance on imports for semiconductors.

The fact that China is growing & has cheap labour helps too.

26/ A final trend is the rise of automated testing equipment. As chips get more complex, the testing must go beyond just spotting defects and towards results assessment and modification – making chips more niche specific.

27/ Thanks for coming to my TED talk.